Counterparty Risk and the Establishment of the NYSE Clearinghouse, (Asaf Bernstein, Eric Hughson and, Marc Weidenmier).

[PDF]

Abstract

The recent financial crisis suggests that counterparty risk in markets without multilateral net settlement through a centralized clearing party (CCP) may pose a threat to financial stability. We study the effect of clearing on counterparty risk by examining a unique historical experiment, the establishment of a clearinghouse on the New York Stock Exchange (NYSE) in 1892. During this period, the largest NYSE stocks were also listed on the Consolidated Stock Exchange (CSE), which already had a clearinghouse netting trades. Using identical securities on the CSE as a control, we find that the introduction of netting on the NYSE reduced the average counterparty risk premium by 24bps and volatility by 26-42bps. Prior to clearing, shocks to overnight lending rates reduced the value of stocks on the NYSE, relative to identical stocks on the CSE, but this was no longer true after the establishment of clearing. We also show that at least ½ of the average reduction in counterparty risk is driven by a reduction in contagion risk through spillovers in the trader network. Our results indicate that clearing can cause a significant improvement in market stability and value through a reduction in network contagion and the counterparty risk premium.

Outsourcing through Purchase Contracts and Firm Capital Structure, (Katie Moon and Gordon Phillips).

[PDF]

Abstract

We examine firm and industry characteristics associated with outsourcing and the relation between outsourcing and capital structure using a unique database of purchase contracts for a measure of firm outsourcing. We document firm, industry, and supplier characteristics that are significantly associated with outside purchase contracting. We find that supplier competition and distance impact the use of purchase contracts, along with firm growth options and value-added per worker. Examining the outside purchase contract and leverage decisions using simultaneous equations, we find that firms in competitive industries, with more growth options, that have suppliers farther away with highercompetition are more likely to use purchase contracts but have less leverage. Our results are consistent with firms that choose to use purchase contracts using less leverage to mitigate the potential loss of relationship-specific investments of contacting parties that can occur with financial distress or bankruptcy.

Friends during Hard Times: Evidence from the Great Depression, (Diego Garcia, Tania Babina, and Geoff Tate).

[PDF]

Abstract

We test whether network connections to other firms through executives and directors increase value by exploiting differences in survival rates in response to a common negative shock. We find that firms that had more connections on the eve of the 1929 financial market crash have higher 10-year survival rates during the Great Depression. Consistent with a financing channel, we find that the results are particularly strong for small firms, private firms and firms with small cash holdings relative to the sample median prior to the shock. Moreover, connections to cash-rich firms are stronger predictors of survival, overall and among financially constrained firms. Because of the greater segmentation of markets in the 1920s and 1930s than in modern data samples, we can mitigate the potential endogeneity of network connections at the time of the shock by exploiting variation in the local demand for directors’ services. We also find evidence that the information that flows through network links increases the odds that a firm will be acquired.

Costs of Rating-Contingent Regulation: Evidence from the Establishment of “Investment Grade”. (Asaf Bernstein)

[PDF]

Abstract

I assess unintended consequences for non-financial firms of rating-contingent regulation, without confounding factors prevalent in modern markets, by examining the 1936 unexpected inception of federal bank investment restrictions for bonds rated below investment grade. Using a difference-in-differences design, I find a persistent rise in speculative bond yields, even comparing bonds within the same firm, and declines in equity value and idiosyncratic volatility for firms reliant on external speculative debt financing. The increase in yields is lower for bonds near investment grade suggesting firms reduce volatility and deviate from otherwise optimal behavior to avoid higher funding costs from the regulation.

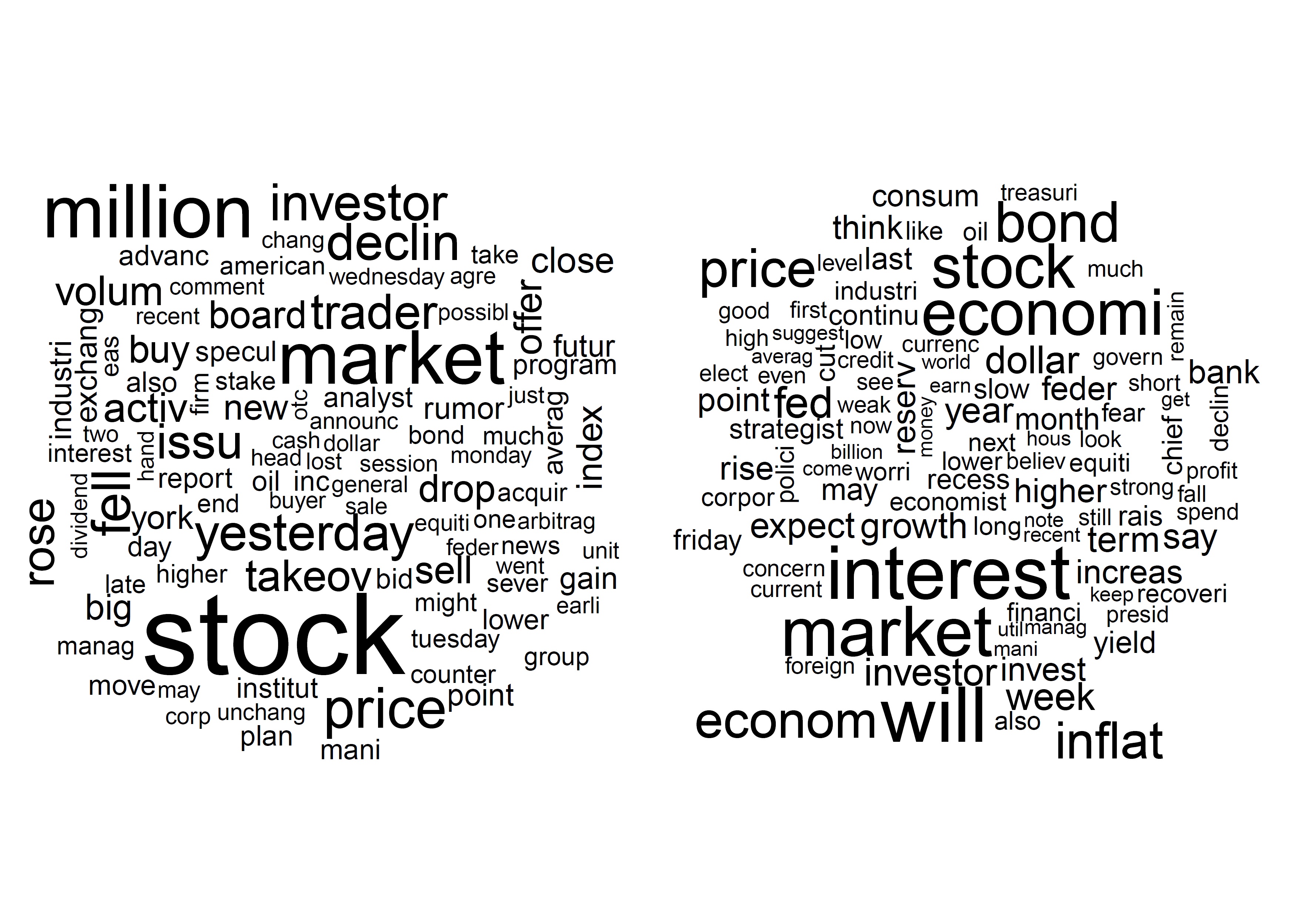

The kinks of financial journalism. (Diego Garcia)

[PDF]

Abstract

This paper studies the content of financial news as a function of past market returns. As a proxy for media content we use positive and negative word counts from general financial news columns from the Wall Street Journal and the New York Times. Our empirical analysis allows us to discriminate between theories that predict hyping good stock performance to those that emphasize negative news. The evidence is conclusive: negative market returns taint the ink of typewriters, while positive returns barely do. Given how pervasive our estimates are across multiple time periods, subject to different competitive pressures in the market for news, we conclude our results are driven by demand considerations.

Innovation in Mature Firms: A Text-Based Analysis. (Tony Cookson, Gustaf Bellstam, and Sanjai Bhagat)

[PDF]

Abstract

We develop a new measure of innovation using a textual analysis of analyst reports. Our text-based measure gives a useful description of innovation by mature firms with and without patenting and R&D. For non-patenting firms, the measure identifies firms that adopt novel technologies and innovative business practices (e.g., Walmart’s cross-geography logistics). For patenting firms, the text-based measure strongly correlates with valuable patents, which likely capture true innovation. The text-based measure robustly forecasts greater firm performance and growth opportunities for up to four years, and these value implications hold just as strongly for non-patenting firms.

Do Economists Swing for the Fences after Tenure?. (Jonathan Brogaard, Joseph Engelberg and Edward Van Wesep)

[PDF]

Abstract

Using a sample of all academics who pass through top 50 economics and finance departments from 1996 through 2014, we study whether the granting of tenure leads faculty to pursue riskier ideas. We use the extreme tails of ex-post citations as our measure of risk and find that both the number of publications and the portion consisting of “home runs” peak at tenure and fall steadily for a decade thereafter. Similar patterns hold for faculty at elite (top 10) institutions and for faculty who take differing time to tenure. We find the opposite pattern among poorly-cited publications: their numbers rise steadily both pre- and post-tenure.